{kind=link}

Last week, I presented a model of a migrant’s road to financial stability, which is composed of two stages: Achieving Independence and then Achieving Stability. All of this is based on two precipitating conditions: an indebted road to migration and a home bias for investing. Today we detail how to achieve financial independence. Although this study is specific to poorer population of migrants, there is a lot to learn for all other members of society.

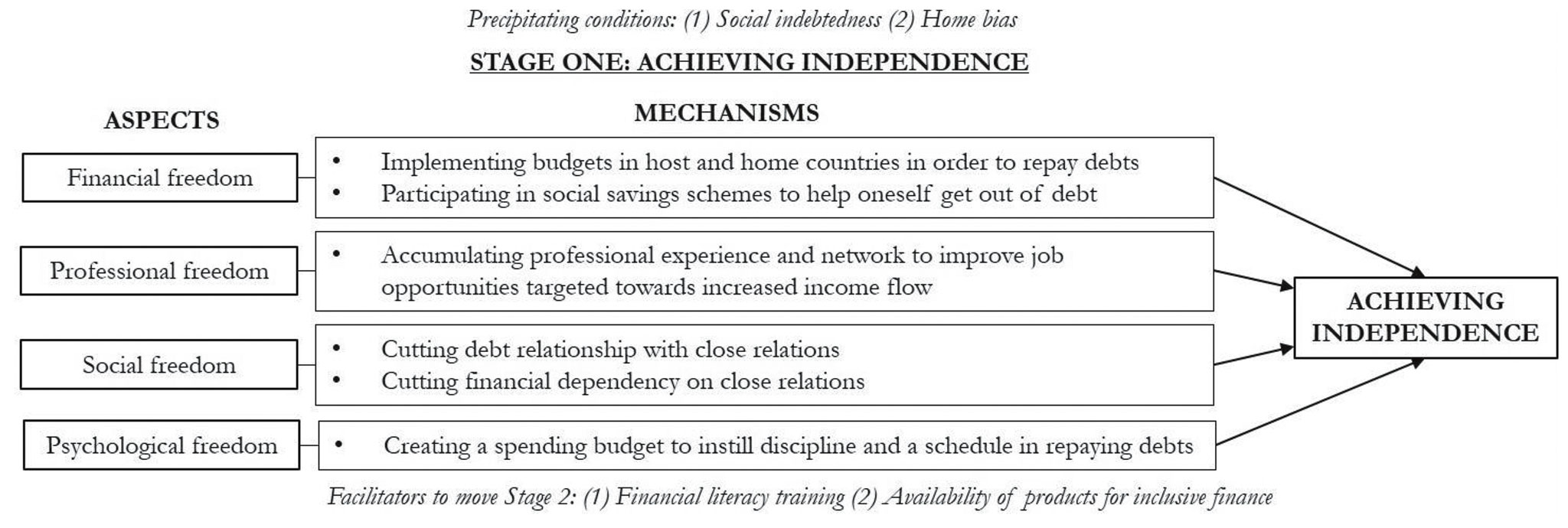

Financial freedom. I found that in order to achieve financial independence, one needs more than simply financial freedom, although this is the most obvious thing to consider. The default situation of indebtedness is what largely structures the migrants’ strategies and behaviors during the first few years abroad, in that everything they do is targeted at paying off their debts. This was true even when such loans bore no interest or had no strict deadline. They implemented strict budgets both in the host and home countries, often sacrificing daily necessities for the sake of setting aside money for debts. To achieve this, they relied upon a series of mechanisms to impose discipline on accumulating lump sums such as joining the rotating credit scheme we have seen in Microfinance called the paluwagan, which put social pressure to save.

Professional freedom. At the beginning stages of migration, a migrant is at the mercy of his or her employer or employers. In domestic work, references and recommendations are key, and given the short-term nature of the work, networking is essential to getting more work. During this period, many employers are abusive and do not pay the social security fees for the migrant or provide a low salary knowing that the person is desperate for work and has debts to pay. The migrant thus concentrates efforts on accumulating professional experience and her network to improve job opportunities targeted towards increased income flow. For several months, they do not do other activities other than work, work overtime, and accept odd or thankless jobs.

{kind=link}

Social freedom. Above and beyond simply having a financial debt to work for and pay off, however, is the social aspect attached to the debt and the relationships that could suffer because of this pressure. When one is poor, relationships matter all the more. Maintaining good relationships is the key motivator for migrants to pay off their debts as soon as possible.

“My reason why I want to settle everything, is because — true or not — it’s as though I feel that the way I am treated by my debtors is not the same as before, now that I owe them money.” (Eduardo)

The first means to repair or at least not put a relationship in jeopardy is to pay the debts as soon as possible and to cut the debt relationship with the closest relatives. This reduces their dependency on people, allowing them to have social freedom and gain acceptance once again.

Psychological freedom. Finally, migrants felt psychologically imprisoned by the debt which caused them depression and demotivation.

“You know, people with debts, even before sleeping, I don’t know if you have experienced it already… before closing one’s eyes, the problem of the debt is on your mind. And even before having opened your eyes (in the morning), it is on your mind again. It’s that hard. (Eduardo)

FACILITATORS TO MOVE TO STAGE 2

Though many migrants could normally get out of the debt within two to three years by working hard, many of them remained indebted or in a very unstable financial situation despite their improved resources. There was only one explanation for this: they felt the need to repay moral debts, what in Filipino is called utang na loob. This meant that whenever a person approached them for money, they found it difficult to refuse. They not only felt the need to help each other out, but they want to do this; this is their source of success and joy.

“I am very good at listing things when it comes to what I owe, but when it comes to the things I give, I don’t list that down.” (Jenalyn)

To counteract this strongly embedded cultural norm, two facilitators are needed in order for a migrant to shift from being independent to achieving stability. These are financial literacy training and the availability of products for inclusive finance.

Financial literacy training. I perused survey data from the Leadership and Social Entrepreneurship program of the Ateneo de Manila University, a program which teaches leadership, financial literacy, and social entrepreneurship to migrants across 10 countries. One of the key highlights of the survey is that after financial literacy training, participants were more aware of setting limits to remittances or “giveaways” to friends and relations.

Availability of products for inclusive finance. Another key facilitator was the fact that traditional banking in France was largely inclusive even to migrants with no papers. Anyone could open a bank account with savings accounts and even create home savings schemes. Having a bank account was necessary to be able to do any future transaction in France and migrants quickly adapted to the system.

When we talk about financial independence, it is not just having an income to support oneself or being free from debt. It is the combination of financial, professional, social, and psychological freedom. And yet this still may not lead to financial stability because of cultural impediments or unforeseen circumstances. To move to that next stage, financial literacy and inclusive finance remain key.

Daniela “Danie” Luz Laurel is a business journalist and anchor-producer of BusinessWorld Live on One News, formerly Bloomberg TV Philippines. Prior to this, she was a permanent professor of Finance at IÉSEG School of Management in Paris and maintains teaching affiliations at IÉSEG and the Ateneo School of Government. She has also worked as an investment banker in The Netherlands. Ms. Laurel holds a Ph.D. in Management Engineering with concentrations in Finance and Accounting from the Politecnico di Milano in Italy and an MBA from the Universidad Carlos III de Madrid.