{kind=link}

With esteemed financial practitioners and good friends, BDO Capital President Ed Francisco and ING Bank President Hans Sicat, I was recently asked to be a panelist in a Philippine Daily Inquirer 35th Anniversary forum. That question, the title of this piece, was posed by our moderator, Business Editor Tina Arceo-Dumlao.

Save for minor variations, we gave similar answers which I paraphrase thus: “Yes, we will see some bounce back, but largely due to base effects from the depressingly low level this year, and we won’t be seeing the Philippine economy back to 2019 levels until 2022 at the earliest. The recovery shape won’t be a V, may not even be a Nike swoosh or a U, but more like a ‘dirty L’ (Han’s depiction) with features of a K, uneven across industries, firms, and the populace.”

Characterizing the crisis as unprecedented and whose impact is sudden, severe, and globally synchronous, I was the most pessimistic among us three. I echoed what we wrote for GlobalSource Partners of a bounce back to only 5% next year, after a severe contraction of 9.5% this year. Moreover, that medium term growth is unlikely to recover to the six to seven percent range of the recent past seven years, and more likely to struggle at four to five percent, closer to the long-term growth record of the Philippines.

I mentioned the following reasons for my pessimism:

1. Risk of more infections and stricter quarantines, possible second or third waves: Notwithstanding success in flattening of the infection curve recently that has allowed some easing of the longest and strictest lockdowns.

This is thanks to the notable augmentation of Department of Health efforts by heavy hitters Secretary Charlie Galvez as National Task Force Chief Implementor, Secretary Vince Dizon as his Deputy, the three other czars (for testing, tracing, and quarantine facilities), and Presidential Adviser Joey Concepcion. They have also commendably mobilized the massive support of the private sector, too numerous to enumerate here, in what everyone appreciated to be an existential national undertaking.

However, major gaps exist including execution of a more digital tracing system, much delayed payments by Philhealth to labs and hospitals, and vaccine procurement where the Philippines is unfortunately at the end of the queue.

An expert I consulted considered that only 25% to 50% of our 108 million population are likely be inoculated by the end of 2022, a good two years away; quite understandable considering how massive and unprecedented such an undertaking is with enormous uncertainties on the approval process, which vaccines will work, for how long, inadequate cold chain and other logistical infrastructure, and the willingness of people to queue up given concerns over unknown long-term side effects. The fairly recent controversies regarding the anti-dengue vaccination program of the last administration is a further dampener.

This all means that physical distancing as a policy to prevent a resurgence in sickness will need to remain in place, especially in dense metropolitan areas that also account for a large share of output, as well as continuing constraints in public transportation and fearful public behavior.

Which brings us to the next concern.

2. Lack of domestic demand.

a. Household consumption which accounts for 70% of GDP has dropped sharply, notwithstanding Government cash transfers and wage subsidies in the hundreds of millions. A World Bank survey in August revealed that 24% of household heads employed in February were no longer working in August and of those still working, 57% reported reduced or no income. A separate Bangko Sentral ng Pilipinas (BSP) consumer survey also showed that the share of households with savings dropped from 38% to 25%. Meanwhile, the latest consumer and business sentiments showed negative indices, meaning pessimists outnumber optimists.

b. Investments have also plummeted. Reports indicate that firms have underutilized capacities with poor earnings prospects, with certain conglomerates mulling further cuts in capital expenditures next year. The World Bank July 2020 firm survey showed that 15% of over 74,000 respondents had permanently closed down, 40% had temporarily suspended operations (evenly split between voluntary and by government mandate), and job losses had been extensive with 48% of firms having laid off workers, especially in education, food services, and construction. (Uncertainties related to post 2022 national elections are a further reason for firms to “wait and see.”)

We also need to be mindful of “scarring,” output losses that are permanent due to damage to medium-term supply potential such as bankruptcies, lower labor force participation from skills mismatch, impact on human capital due to disruptions in school attendance and health services, and obstacles to resource allocation such as supply chain disruptions.

3. Policy constraints.

a. Monetary policy has been timely and vigorous in providing the needed liquidity shot in the arm. But there are limits to monetary policy in lifting demand especially when interest rates are already at low levels, what economists call “pushing on a string.”

Data thus far validate this. The BSP as of Oct. 27 had already injected P1.9 trillion into the financial system through its set of accommodative policy actions. But banks have understandably been cautious, mindful of their fiduciary responsibility to depositors who provide the bulk of their loanable funds. At the end of Q3, net domestic credits to the private sector increased by only 1.4% year on year compared with a 12% growth in M3. Meanwhile, monies parked in the BSP’s deposit facilities stood at over P1.2 trillion as of end October compared with less than P400 billion at the end of the first quarter.

The one area where the BSP can perhaps be more aggressive is in arresting the further appreciation of the peso, the only currency in our region that appreciated vs the dollar, by doing even more market interventions. This will help our exporters, OFW families, and support overall aggregate demand.

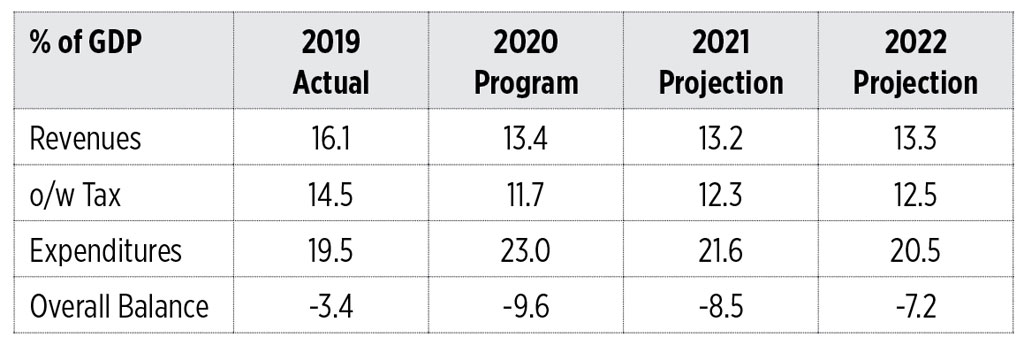

b. Fiscal policy. Spending so far has been “middle of the pack” versus other countries. The Department of Finance’s announced policy to “keep our powder dry” is meant to ensure that we do not compromise needed future access to finance. Already, programmed deficits for the next two years are estimated at seven to nine percent of GDP, two to three times normal prudent levels, and there is much uncertainty on how long this plague will last.

Moreover, I believe current spending has been constrained not so much by the size of the budget, but by limitations on: a.) distribution of income and wage support absent a national ID system that will enable “ayuda” with minimum of leakage; and, b.) slow releases and execution of projects, as shown in the poor disbursements of capital outlays.

The soon to be signed CREATE (Corporate Recovery and Tax Incentives for Enterprises) bill which lowers corporate income taxes and rationalizes fiscal incentives will also provide immediate stimulus equivalent to over P250 billion in the next two years. This does not count the favorable effects this long delayed structural reform will have in generating more investments, both foreign and local. (I congratulate Secretary Dominguez and Secretary Chua and the sponsors of the bill for bringing this landmark reform to the finish line, building on the efforts of their predecessors, who publicly supported this bill).

Against this dour prognosis I also mentioned some green shoots which we all wish will bring early spring:

1. The unveiling of several vaccines and their much earlier roll out in rich country trading partners which will have some trade, remittance, and investment spillovers to us;

2. The robustness of our BPO sector which has nimbly adopted working from home thanks also to our telco service providers;

3. The surprising resilience of remittances which only declined by 1.4% in the year to September;

4. Some evidence of “revenge spending” by those in the upper leg of the K curve; and,

5. Accelerated investments all around in digital technology.

I ended my remarks by saying, despite having a good track record in forecasting output growth, this is the one time I would love to be terribly wrong. And I quoted noted economist John Kenneth Galbraith: “The only function of economic forecasting is to make astrology look respectable.”

Romeo L. Bernardo was finance undersecretary during the Cory Aquino and Fidel Ramos administrations. He is a Board Trustee/Director of the Foundation for Economic Freedom, the Management Association of the Philippines, and the FINEX Foundation.